Eldorado Resorts’ Fourth Quarter Combined Net Revenue Rises 2.3% to $214.3 Million and Combined Adjusted EBITDA Increases 21.1% to $32.2 Million

- Full Year 2015 Combined Net Revenue for Eldorado Resorts, Silver Legacy and Circus Circus Reno Totaled $901.5 Million with Adjusted EBITDA of $160.2 Million

Eldorado Resorts, Inc. 2 minutes ago

RENO, Nev.--(BUSINESS WIRE)--

Eldorado Resorts, Inc. (

ERI) (“Eldorado,” “ERI,” or “the Company”) today reported operating results for the three and twelve months ended December 31, 2015. Net revenues and Adjusted EBITDA for all periods summarized below include the operations of Silver Legacy and Circus Circus Reno, which were acquired by ERI on November 24, 2015 (“the Acquisition Date”), as if the acquisition occurred on January 1, 2014 and the operations of MTR Gaming Group, Inc. (“MTR”), which merged with the Company on September 19, 2014 (“the Merger Date”), as if the merger occurred on January 1, 2014.

| | | | | | | | | | | | | | | | | | | | | | | | | �

| ($ in thousands) | | | Total Net Revenue | | | Total Net Revenue | | | | | | | | | | | | | | | | | | | �

| | | Three Months Ended | | | Twelve Months Ended | | | | | | | | | | | | | | | | | | | �

| | | December 31, | | | December 31, | | | | | | | | | | | | | | | | | | | �

| | | | 2015 | | | | 2014 | | | Change | | | | 2015 | | | | 2014 | | | Change | | | �

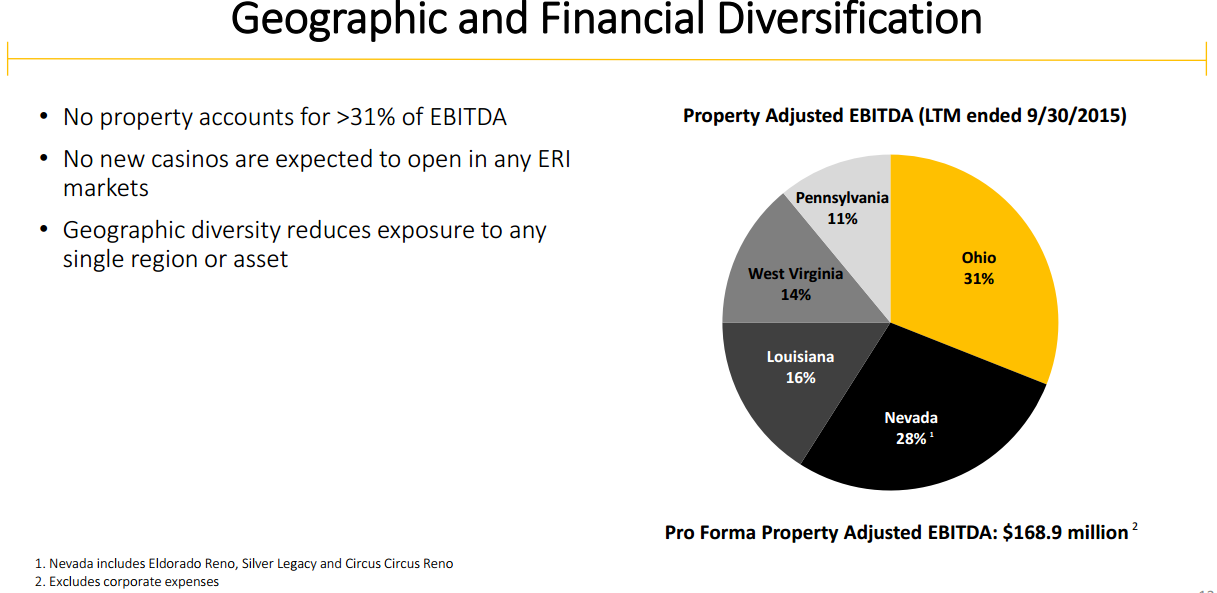

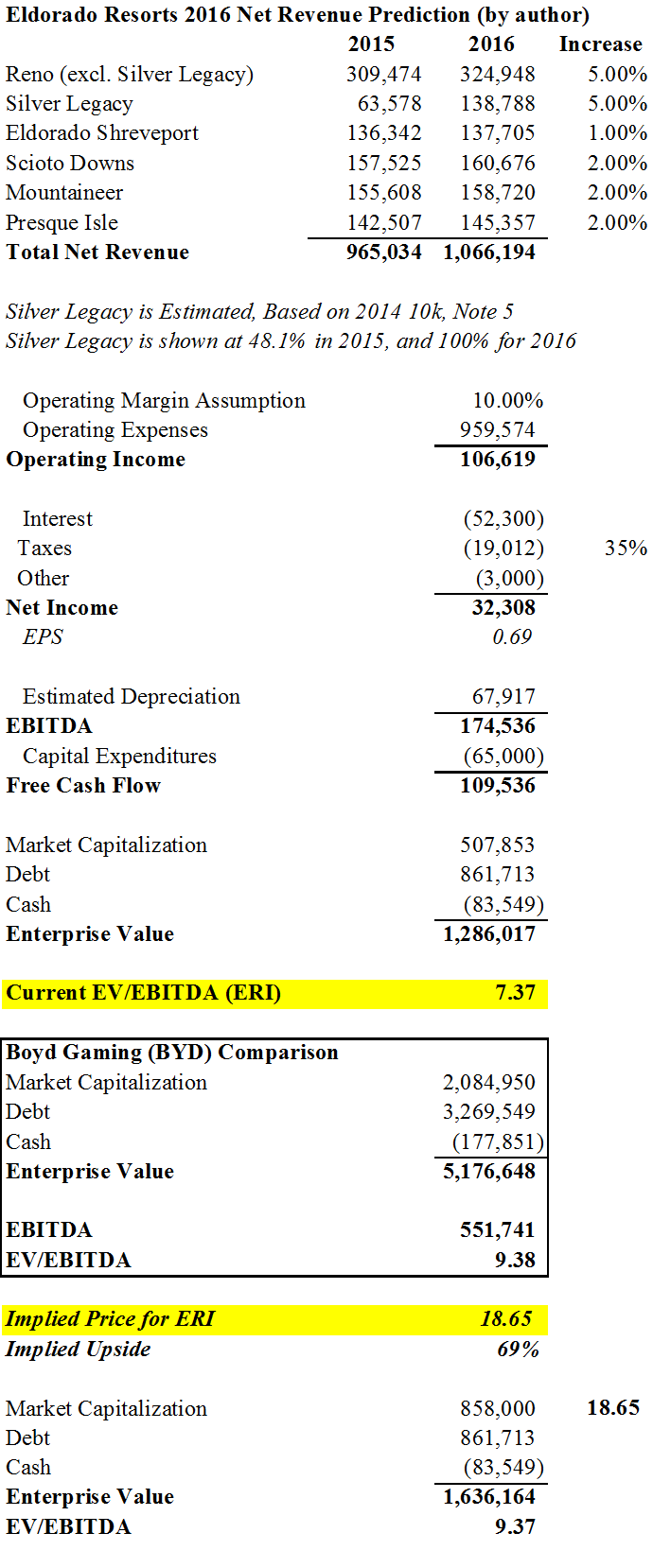

| Reno Tri-Properties (1) | | | $ | 76,010 | | | $ | 69,901 | | | 8.7 | % | | | $ | 309,474 | | | $ | 298,410 | | | 3.7 | % |

| Eldorado Shreveport | | | | 32,422 | | | | 31,838 | | | 1.8 | % | | | | 136,342 | | | | 133,960 | | | 1.8 | % |

| Scioto Downs | | | | 39,087 | | | | 35,329 | | | 10.6 | % | | | | 157,525 | | | | 148,480 | | | 6.1 | % |

| Mountaineer | | | | 32,989 | | | | 40,057 | | | (17.6 | )% | | | | 155,608 | | | | 184,848 | | | (15.8 | )% |

| Presque Isle Downs | | | | 33,820 | | | | 32,471 | | | 4.2 | % | | | | 142,507 | | | | 142,717 | | | (0.1 | )% |

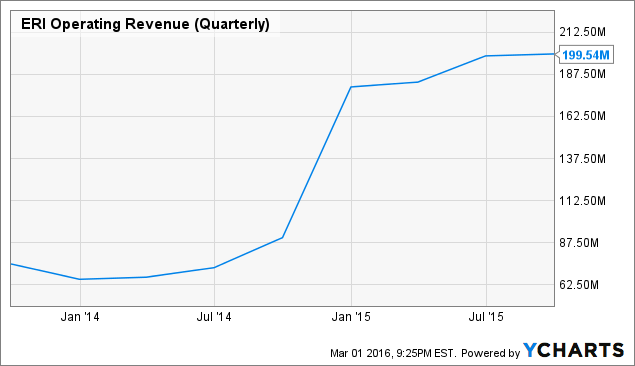

| Total Net Revenue (4) | | | $ | 214,328 | | | $ | 209,596 | | | 2.3 | % | | | $ | 901,456 | | | $ | 908,415 | | | (0.8 | )% |

| | | | | | | | | | | | | | | | | | | | | | | | | �

| ($ in thousands) | | Adjusted EBITDA | | Adjusted EBITDA | | | | | | | | | | | | | | | | | | | �

| | Three Months Ended | | Twelve Months Ended | | | | | | | | | | | | | | | | | | | �

| | December 31, | | December 31, | | | | | | | | | | | | | | | | | | | �

| | | 2015 | | | | 2014 | | | Change | | | 2015 | | | | 2014 | | | Change | | | �

| Reno Tri-Properties (1) (2) | | $ | 9,030 | | | $ | 5,812 | | | 55.4 | % | | $ | 49,939 | | | $ | 35,335 | | | 41.3 | % |

| Eldorado Shreveport | | | 6,324 | | | | 4,158 | | | 52.1 | % | | | 29,026 | | | | 24,142 | | | 20.2 | % |

| Scioto Downs | | | 12,720 | | | | 11,551 | | | 10.1 | % | | | 53,980 | | | | 49,345 | | | 9.4 | % |

| Mountaineer | | | 2,714 | | | | 5,240 | | | (48.2 | )% | | | 21,268 | | | | 30,412 | | | (30.1 | )% |

| Presque Isle Downs | | | 5,248 | | | | 3,670 | | | 43.0 | % | | | 20,311 | | | | 19,415 | | | 4.6 | % |

| Corporate | | | (3,806 | ) | | | (3,818 | ) | | (0.3 | )% | | | (14,364 | ) | | | (12,022 | ) | | 19.5 | % |

| Total Adjusted EBITDA (3) (4) | | $ | 32,230 | | | $ | 26,613 | | | 21.1 | % | | $ | 160,160 | | | $ | 146,627 | | | 9.2 | % |

| | | | | | | | | | | | | | | | | | | | | | |

| (1) | | Reno Tri-Properties includes the operations of Eldorado Reno, Silver Legacy and Circus Circus Reno for all periods. |

| (2) | | Reno Tri-Properties increase in Adjusted EBITDA for the twelve months ended December 31, 2015 reflects the reallocation of corporate expenses. If corporate expenses had been reallocated in the twelve months ended December 31, 2014, the Adjusted EBITDA percentage increase would have been 30.8%. |

| (3) | | Adjusted EBITDA is not a generally accepted accounting principle ("GAAP") measurement and is presented solely as a supplemental disclosure because the Company believes it is a widely used measure of operating performance in the gaming industry. See "Reconciliation of GAAP Measures to Non-GAAP Measures" below for a definition of Adjusted EBITDA and a quantitative reconciliation of Adjusted EBITDA to net (loss) income, which the Company believes is the most comparable financial measure calculated in accordance with GAAP. |

| (4) | | The combined basis reflects operations of MTR for periods prior to the merger and Silver Legacy and Circus Circus Reno prior to the acquisition combined with the operations of Eldorado Resorts, Inc. Such presentation does not conform with GAAP or the Securities and Exchange Commission rules for pro forma presentation; however, we have included the combined information because we believe it provides a meaningful comparison for the periods presented. |

“Eldorado’s strong fourth quarter and full year financial results mark the conclusion of another successful and active year for the Company. With fourth quarter revenue and EBITDA gains at all but one of our properties, Eldorado’s consolidated Adjusted EBITDA rose 21.1%. Furthermore, with Adjusted EBITDA growth of more than 10% at six of our seven properties, the strength across our portfolio in the fourth quarter was broad based. Our fourth quarter and full year adjusted EBITDA margin growth reflects the impact of property enhancement initiatives that target product and service offering upgrades across our entire portfolio while exercising cost discipline and extracting operating efficiencies. For example, the opening of

The Brew Brothers, our restaurant and microbrewery at Scioto Downs, drove a meaningful increase in traffic and slot revenues. We believe our continued focus on margin expansion combined with the strength of our properties in their respective markets provides a basis for continued near- and long-term financial growth and the enhancement of shareholder value,” said Gary Carano, Chairman and Chief Executive Officer of Eldorado.

“During the quarter we closed on the acquisition of the 50% of Silver Legacy and all of the assets of Circus Circus Reno which was immediately accretive to our free cash flow. The acquisition of these properties complements our already strong position in downtown Reno and is consistent with our strategy to expand our scale through strategic, accretive transactions. Eldorado’s Tri-Property Reno complex completed an extraordinary year, with fourth quarter Adjusted EBITDA growth of 55.4%.

“2015 was a transformative year for Eldorado as we fully integrated MTR Gaming’s operations into the Eldorado portfolio and completed significant enhancements through prudent, return-focused capital allocation at each of our properties. At Scioto Downs, we built and opened

The Brew Brothers. At Presque Isle Downs and Casino, we completed the $5.0 million five-phase design and facility enhancement program that added a new casino center bar, an improved high limit gaming area and exciting new slot product. At Eldorado Reno, over 200 rooms were remodeled and we completely refurbished the exterior of Eldorado Shreveport. At Mountaineer Casino, Racetrack & Resort, a new smoking patio was added with 261 slot machines and six table games. We are excited as we look forward to 2016, especially in the Reno market as job growth for Northern Nevada is projected to more than double the historical average. We are pleased to report that our operating momentum has continued in the first quarter.”

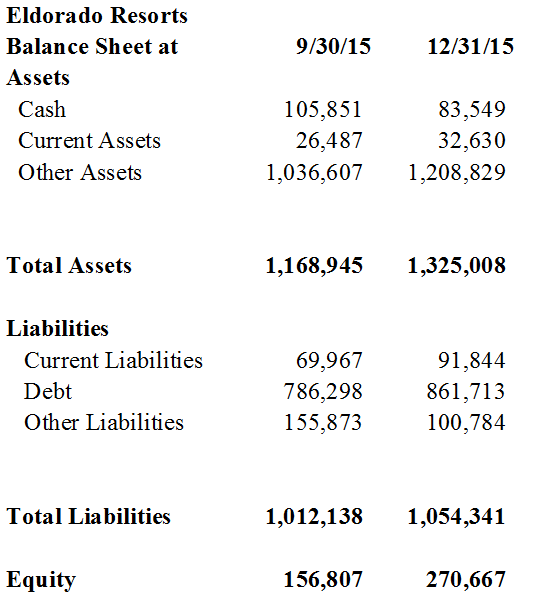

Balance Sheet and Liquidity

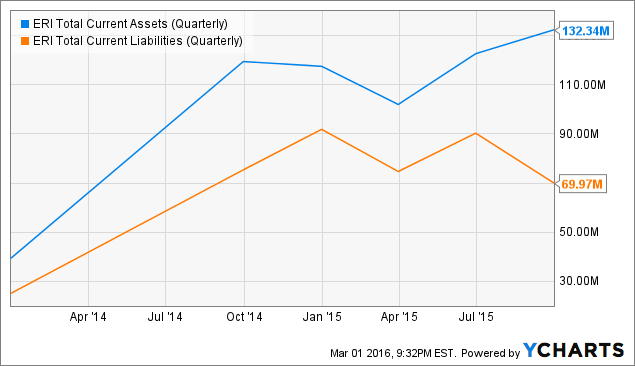

At December 31, 2015, Eldorado had $78.3 million in cash and cash equivalents and $5.3 million in restricted cash. Outstanding indebtedness at December 31, 2015 totaled $891.4 million, including $93.5 million outstanding on the Company’s revolving credit facility. We spent $11.0 million in capital expenditures in the fourth quarter, and $35.5 million for all of 2015. We anticipate capital spending of $50 million in 2016, with approximately $15 million allocated to project cap-ex and the remaining $35 million for maintenance cap-ex.

“After careful review of our financing options for the Silver Legacy and Circus Circus Reno acquisition, we chose to fund the final piece of the transaction with existing revolver capacity, in lieu of an equity offering,” said Tom Reeg, President of Eldorado. “We remain committed to reducing our debt in 2016 with free cash flow, as we realize revenue and cost synergies across the Reno Tri-Properties. Our announced cost savings program has been a success as we both exceeded our projected $10 million target of annual cost savings, and did so a full quarter ahead of plan. Our cost savings helped drive an Adjusted EBITDA margin increase of approximately 230 basis points in the fourth quarter.”

Summary of 2015 Fourth Quarter Property Results and Facility Enhancements

Nevada

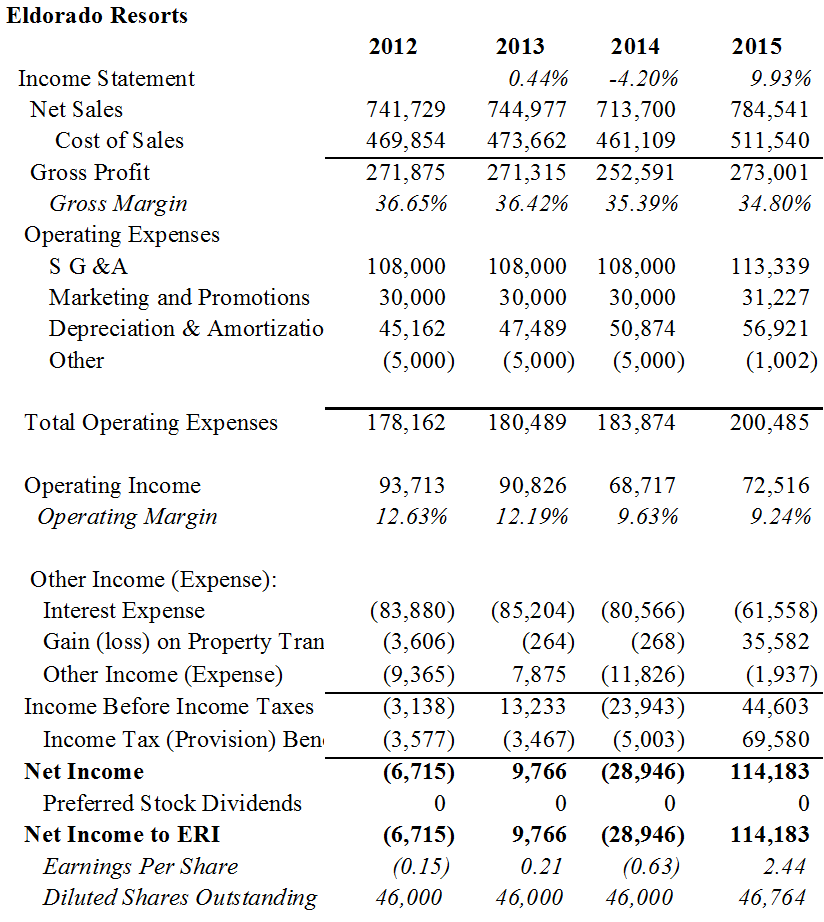

Net revenues of $76.0 million at the Reno Tri-Properties for the quarter ended December 31, 2015 increased 8.7% over the prior-year period while Adjusted EBITDA of $9.0 million increased 55.4% from the same period in 2014. The increased revenue and Adjusted EBITDA were driven by increased casino volumes as well as increased occupancy and a higher ADR. Eldorado Reno’s performance also reflects the Company’s expense management programs and we expect to generate further revenue and expense synergies across the three properties in 2016. The Northern Nevada economy continues to prosper as taxable sales rose by 8.2% in 2015 compared to the prior year, while single-family homes sold and the median price increased 14.6% and 15.3%, respectively, over the same time period. Net revenue and Adjusted EBITDA for the fourth quarter 2015 were $47.8 million and $6.9 million, respectively, with the 38 days of operations from Silver Legacy and Circus Circus Reno and full quarter from Eldorado Reno.

Louisiana

Net revenues at Eldorado Shreveport rose 1.8% to $32.4 million in the fourth quarter of 2015. Adjusted EBITDA from the property increased 52.1% to $6.3 million from $4.2 million in the comparable quarter of 2014 with adjusted EBITDA margins increasing by approximately 645 basis points to 19.5%. Reflecting the margin enhancement, Eldorado Shreveport delivered substantial EBITDA growth on a modest revenue gain, despite sustained weakness in energy prices during the fourth quarter and throughout 2015.

Eastern Properties

Net revenues at Scioto Downs Racino increased 10.6% to $39.1 million in the fourth quarter of 2015 from $35.3 million in the fourth quarter of 2014. Scioto Downs’ fourth quarter 2015 Adjusted EBITDA increased 10.1% to $12.7 million from $11.6 million in the comparable prior year period. The addition of

The Brew Brothers microbrewery and restaurant was a key factor in driving additional visitation and slot revenue in the quarter. During the quarter, the property was rebranded as “Eldorado Gaming Scioto Downs” with new signage throughout the facility, including a large pylon sign with an electronic message board in front. Finally, the Company and its joint venture partner broke ground on a 118-room Hampton Inn hotel in October, which is expected to open in the fourth quarter of 2016. We have begun construction of a second smoking patio with 120 new VLTs with a targeted opening date of June 1.

Fourth quarter 2015 net revenues of $33.8 million at Presque Isle Downs & Casino increased 4.2% from $32.5 million in the fourth quarter of 2014. Adjusted EBITDA increased 43.0% to $5.2 million in the fourth quarter of 2015 from $3.7 million in the same comparable quarter with adjusted EBITDA margin rising approximately 420 basis points to 15.5%. Net revenue and adjusted EBITDA benefited from the implementation of marketing strategies that target the local Erie market. Adjusted EBITDA also benefited during the quarter from the cost savings program implemented during the second quarter of 2015.

Net revenues at Mountaineer Casino, Racetrack & Resort declined 17.6% to $33.0 million in the fourth quarter of 2015 from $40.1 million in the fourth quarter of 2014. Adjusted EBITDA from the property declined 48.2% to $2.7 million from $5.2 million in the comparable quarter of 2014. Net revenue and Adjusted EBITDA continues to be impacted by the Hancock County Clean Air Regulation that went into effect July 1, 2015 and prohibits smoking in enclosed public places. The smoking patio at Mountaineer continues to be very well received by patrons and is helping mitigate the impact of the new smoking ban. During the quarter, the Company added 61 slot machines to the smoking patio, bringing the total number of slot machines to 261.

Reconciliation of GAAP Measures to Non-GAAP Measures

Adjusted EBITDA (defined below), a non GAAP financial measure, has been presented as a supplemental disclosure because it is a widely used measure of performance and basis for valuation of companies in our industry and we believe that this non GAAP supplemental information will be helpful in understanding the Company’s ongoing operating results. Adjusted EBITDA represents operating income (loss) before depreciation and amortization, stock based compensation, (gain) loss on the sale or disposal of property, equity in income of unconsolidated affiliates, acquisition charges, S-1 expenses and other regulatory gaming assessment, to the extent that such items existed in the periods presented. Adjusted EBITDA is not a measure of performance or liquidity calculated in accordance with U.S. GAAP, is unaudited and should not be considered an alternative to, or more meaningful than, net income (loss) as an indicator of our operating performance. Uses of cash flows that are not reflected in Adjusted EBITDA include capital expenditures, interest payments, income taxes, debt principal repayments and certain regulatory gaming assessments, which can be significant. As a result, Adjusted EBITDA should not be considered as a measure of our liquidity. Other companies that provide EBITDA information may calculate EBITDA differently than we do. The definition of Adjusted EBITDA may not be the same as the definitions used in any of our debt agreements.

Fourth Quarter Conference Call

Eldorado will host a conference call at 4:30 p.m. ET today. Senior management will discuss the financial results and host a question and answer session. The dial in number for the audio conference call is 719/457-1512, conference ID 4113414 (domestic and international callers). In addition, a live audio webcast of the call will be accessible to the public on Eldorado’s web site,

http://www.eldoradoresorts.com/ and a replay of the webcast will be archived on the site for 90 days following the live event.